Industry commentary: The opportunities and uncertainties for biomethane in the FuelEU Maritime

With the kind support of agriportance

FuelEU Maritime is an EU regulation that prescribes gradually decreasing greenhouse gas limits for the energy sources used in maritime transport in order to promote the decarbonisation of shipping through the use of alternative fuels such as biomethane or eFuels.

When the regulation (EU 2023/1805) came into force at the beginning of 2025, there was a great deal of excitement in the German biomethane market. In a reality characterised by sales bottlenecks, particularly in the transport sector, the maritime application is now generating new hope and attention.

A special feature of the FuelEU Regulation is the calculation of emissions, which are divided into ‘well-to-tank’ and ‘tank-to-wake’, i.e. before and after bunkering. It is particularly important that the ‘well-to-tank’ emissions are calculated on the basis of the RED III methodology, which means that particularly low-emission fuels such as biomethane from farm fertilisers, with GHG values of around -100 gCO₂eq/MJ, could represent a major lever.

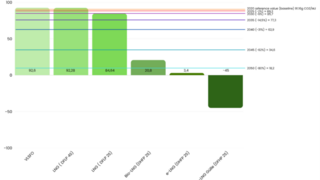

Although the reduction targets are initially rather moderate with a target value of only 2 % by 2030, they increase significantly to 14.5 % by 2035. Another special feature is the fossil reference value of 91.16 gCO₂eq/MJ, which serves as the basis for the savings calculation. This reference value means that even fossil LNG fulfils the requirements under certain conditions. (See figure)

Studies that report significantly higher GHG emissions from LNG during transport and refuelling offer an unfavourable outlook. This could worsen the GHG value by up to +18 gCO₂eq/MJ. This would greatly relativise the supposed advantage of fossil gases, which would also affect bio-LNG.

The question of the recognition of subsidised quantities as part of the fulfilment obligation has not yet been finally decided, but has already been indicated by leaks and statements from the European Maritime Safety Agency (EMSA). If this practice is officially confirmed, non-subsidised producers in Germany in particular will be at a serious competitive disadvantage. Due to existing national subsidy regulations, German players cannot compete on price with subsidised certificates from other European countries.

There is also a discrepancy between European and international recognition of GHG credits for fuel from slurry (esca). While the IMO (International Maritime Organisation) does not provide for the recognition of emission credits from manure in the current draft of its regulations, this is possible at EU level.

Many companies therefore conservatively calculate GHG values of -25 gCO₂eq/MJ, which corresponds to ‘well-to-wake’ emissions of approx. 20 gCO₂eq/MJ. In fact, based on the RED methodology, values of -45 gCO₂eq/MJ would also be realistic. Although this significantly exceeds the future requirements, such as the reduction requirement of 80% by 2050, it is made interesting by two flexibility mechanisms in the regulation: firstly, pooling, in which over-compliant ships can compensate for non-compliant ships from the same operator, and secondly, banking, which allows surplus reductions to be carried forward to subsequent years. These two instruments increase the economic incentive for early investment in low-emission technologies. However, the mechanisms are also criticised as they can lead to a slowdown in structural change by reducing the amount of renewable fuels actually required on the market in the short term. This is similar to the double counting of the GHG quota in road transport, which is now coming to an end.

All in all, FuelEU Maritime certainly opens up new opportunities for the biomethane sector, especially for volumes with highly negative GHG values. Even if mainly subsidised biomethane were to be sold here, these volumes would potentially free up other markets for German producers. It remains to be seen whether the EU Commission will clarify the recognition logic, international compatibility and developments in the emissions calculation logic. It also remains to be seen what impact the GHG quota, which will soon include the shipping sector, will have and how the systems will complement each other.